Market Sentiment: What's the price next month?

Suppose a stock trades at $250. You want to know its price in 30 days. Or

rather, which price is expected in 30 days by most market participants. For this

purpose, Zorro analyzes the chain of 30-day options contracts and calculates a price probability

distribution. The result is the probability of any

future price between $200 and $300 at the option expiration day, based on the

expectations of option buyers and sellers. The most likely price is at the top of

the distribution. The underlying algorithm and usage examples are

described on

financial-hacker.com/the-mechanical-turk.

The following functions estimate

a future price from the current ask, bid, and strike prices of all option

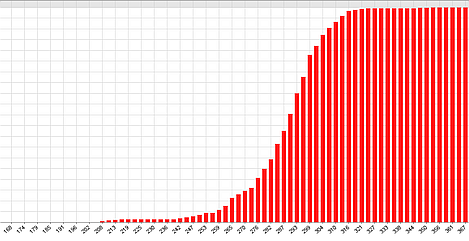

contracts at a determined expiration date. They generate a distribution of the cumulative price probability

at their expiration. The height of a bar in the image below is the probability

that the underlying price will end up at or below the given price level on the x

axis, in the

implied opinion of option traders.

SPY January 2018,

cumulative price probability distribution contractCPD (int Days): int

Generates a cumulative probabililty distribution of the current asset price at

the given number of days in the future, and stores it internally. Returns the

number of option contracts used for the distribution. The

contractUpdate function must be called before.

cpd(var Price): var

Returns the cumulative probability of the given price in 0..100

range.

The future price will be at or below the given

value with the returned probability in percent. The contractCPD

function must be called before.

cpdv(var Percentile): var

Returns the price at the given percentile of the distribution. F.i. cpdv(50)

returns the median of the price distribution, with equal probability of a higher

or lower price. The contractCPD

function must be called before.

Parameters:

| Days |

Minimum number of calendar days for which the price distribution is

estimated. Determines the expiration date of the used options. |

| Price |

Underlying asset price to be estimated. |

| Percentile |

Probability that the future price is at or below the returned value. |

Remarks:

- For comparing price predictions with the current price in the backtest,

make sure to use the unadjusted price. If in doubt, use underlying prices

from the historical options chain by setting History = ".t8";

before selecting the asset.

- contractCPD loads the prices of all contract with the

given expiration and can be very slow with some brokers (up to 30 minutes

with IB). For speeding up price requests, call

brokerCommand(SET_PRICETYPE,8); when supported by the broker.

Example:

void main()

{

StartDate = 20170101;

BarPeriod = 1440;

PlotScale = 10;

assetList("AssetsIB");

assetHistory("SPY",FROM_STOOQ|UNADJUSTED);

asset("SPY");

Multiplier = 100;

// load today's contract chain

contractUpdate(Stock,0,CALL|PUT);

var PriceCurrent = Contracts->fUnl;

printf("\nCurrent price %.2f",PriceCurrent);

// what's the SPY price in 45 days?

contractCPD(45);

var Price = 0.;

int i;

for(i = 0; i < 150; i++) {

Price += 0.01*PriceCurrent;

plotBar("CPD",i,Price,cpd(Price),BARS|LBL2,RED);

}

printf(", projected price %.2f",cpdv(50));

}

See also:

contract, cdf

► latest version online